Global Recession 3.0 – Fasten Your Seatbelts with lessons from India

Shivam Tiwari, country risk underwriter, ECGC Limited.

A general decline in the economic activity in two continuous quarters of a financial year in a country or a region is termed recession. And if that decline in economic activity spills over to other countries and breaches the borders, it gradually takes the form of a global recession that can be triggered by a lot of factors. The current state of the global economy can be attributed directly to two very significant causes - the slowdown caused by the Covid-19 pandemic and the ever-continuing Russia-Ukraine crisis that started in February 2022. The induced effect from these two factors has wreaked havoc on a lot of developing as well as developed economies including the U.S, the European nations and to some extent, the south east Asian economies.

The already slumped economies ravaged by a pandemic were slowly recuperating and pushing on the road to recovery but suddenly a road block in the form of war pushed them again in a whirlpool of economic setbacks.

The war in Ukraine has led to global supply chain crisis that has never been observed in the last 50-60 years. The most important point to note is that Ukraine has been a significant exporter of agricultural goods (oilseeds and grains) and a jolt to that country meant global hunger. In 2021, the total agricultural exports by Ukraine to the World was

$27.8 billion, 41 percent of the country's $68 billion in overall exports. Also, the sanctions by the U.S. and the European Union on Russia resulted into an energy crisis that pushed Europe into a dilemma as well as a crisis.

Inflation – The ‘initiator-in-chief’ of crisis

The synchronized increase in the interest rates by Central banks all over the world in order to balance the galloping inflation presents a very gloomy picture. This is an unprecedented move and has not been done in the last five decades as per the World Bank. This increase in the interest rate is bound to continue in 2023 too however this may not be able to check the rate of inflation.

As per the International Monetary Fund, the multilateral agency that analyses the macroeconomic situation in a country, the pace of monetary tightening is quickening in several countries, particularly in the western advanced economies, in terms of both frequency and magnitude of rate hikes.

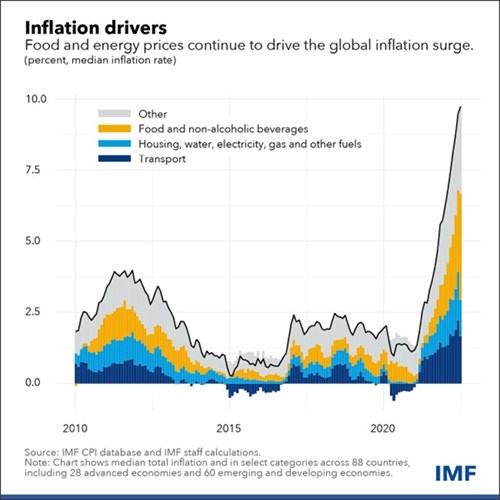

The chart below by the IMF shows that increase in food and energy prices resulting into a global value chain crisis has been one of the main drivers of quickening inflation around the world.

The great fall of Global Real GDP:

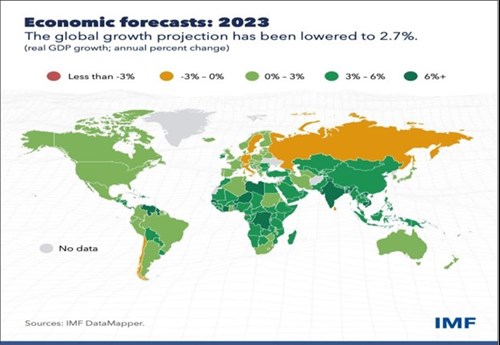

Since the beginning of this year, the global supply chain crisis exacerbated with rising inflation and tightening financial conditions has resulted into many multilateral agencies like the IMF and World bank revising their GDP forecasts for 2023. The IMF has revied its growth forecast to 2.7% in 2023 from 3.2% in 2022.

The real GDP growth rate has been expected to fall to 1.5% from 2.9% in 2022, a notional figure that may catapult any country into macroeconomic troubles of a huge scale.

The direct consequence of the fall in GDP triggers a series of events that results in a general rise in the unemployment rate as well as reduction in the production of essential goods and services. In developing and emerging markets, this leads to a huge gap in income inequality thereby affecting the livelihoods of millions of people.

The below chart from IMF gives an idea of the growth forecast in 2023:

Impact on Employment:

During the financial crisis of 2008-09, the total jobs lost were to the tune of almost 14 million. Though the scale of loss in employment will not be that high in the current situation, a significant erosion in employment levels is nevertheless, expected.

Major layoffs signifies cost cutting amid slowdown

- The Indian case – As of date, 44 start-ups have laid off almost 16,000 employees in the last 3 months. These companies include some big names which are very highly valued. This is just the tip of the iceberg and there may be hundred and thousands of pink slips on the way in the near

- The Global Scale – More than 1,50,000 people have been laid off in the last 3 months in just the western economies, mainly the U.S.A (90,000). Amongst that, Meta (parent company of Facebook) recently announced to slash 11,000 jobs while Twitter terminated 5,600 people from the These are just

preliminary figures and a clearer picture will be available during the early part of 2023.

India – A Peculiar and Resilient case

Though the world order is on the brink of an economic meltdown, it seems the Indian waters are somewhat stable. Although inflation is at a considerably higher level than the target adopted by the Reserve bank of India, its policies along with the economic reforms of the Central Government have done a remarkable job to keep the situation under control. The past trends are a testimony to the fact that the hawkish stance of the India’s central bank has been effective in reigning the galloping inflation.

As the World Economy has become more global and connected, India will not be totally unfazed by the recessionary phase. The recession in U.S and the European countries will have an impact on the Indian subcontinent, though not at the scale that other countries might witness.

The major reasons that are attributable that might keep the Indian Economy balanced are:

- Inward looking economy – The humongous population of India constitute colossal demand addressing the mismatch between the supply glut observed elsewhere and the local consumption. Instead of driving the economic growth cycle through exports during the pandemic years, the domestic consumption has scaled up to shape the growth in the GDP of India. This continues to subside a lot of headwinds that would have adversely affected the economic growth prospects of the

- Demand Pull and Cost Push Inflation – This is one of the most important factors that will help India in the short as well as the long-run. In the economic parlance, the demand-pull inflation happens when the aggregate demand in an economy is greater than the total supply of goods and services while the cost- push inflation takes place when the demand does not change but there is a dearth in the supply-side due to some external factors. In the current case of world-wide inflationary trends, the general observation is that the inflation is a

cost-push inflation as the global supply chain has been hampered by a number of factors starting from the pandemic, the geopolitical crisis, the euro-zone energy crisis and the resultant upheavals in the trade patterns.

Considering all these factors, India is at a juncture where all its supply needs have been satiated by its significant trade partners. Considering the fact the major import bill of India comprises of Mineral Oil and related products, the mechanism adopted by India to secure its supplies with its trading partners has been able to cater to the domestic demand without any significant supply chain disruptions.

As a result, inflation has largely been tamed by the monetary authority i.e the RBI.

- Robust trend in Exports– As per the data by the Ministry of Commerce, India’s overall exports (Services and Merchandise) touched USD 2 Billion in financial year 2021-2022 showing an increase of almost 38% as compared to 2020-21. These figures give an idea that the country is performing despite global headwinds.

Though we may be optimistic about India’s future economic course, we must not be overly-optimistic. The policies of the Government must incorporate the changes as and when necessary and needed. As the world suffered during the pandemic, this recessionary phase has given subtle hints that it might happen again and it would be further aggravated by multitude of factors.

Till then, fasten your seatbelts. The journey might be slightly turbulent, if not much.